If quoting or using this article by any other means, a link back to it must be included. A credit to the author and original publication must be provided as well, by adding the following reference: Litvinenko V. S. Digital Economy as a Factor in the Technological Development of the Mineral Sector/Natural Resources Research, №28, Т 28, 2019. С 1-21.

Saint-Petersburg Mining University, Saint Petersburg, Russia

V. S. Litvinenko

Abstract

This article describes the impact of the global digital economy on the technological development of the mineral sector in the world. Due to the different specifics of the legislative bases of the investigated regions, such as the USA, China, EU, and Africa, the development of digital transformation is presented on the example of the Russian Federation in the context of world trends. The article presents an analysis of the possibilities of using straight-through digital technology in prospecting, design, development, and use of mineral resources. It describes a structure promoting the development of applied digital technology through research–education centers and international competence centers. This structure would allow forming the new competencies for personnel working in the digital economy. The underfunding of the information and computing infrastructure could be a significant challenge to the digital transformation of the economy. Creating the conditions for a reliable and secure process of generating, storing, and using data is the basis for protection from the cybersecurity hazard that could act as a brake on technology advancement. This article discusses the organizational and technological priorities of the development of the mineral resource sector on the example of the Russian Federation. The challenges for the mineral resource complex resulting from global changes can be taken on through technological changes of the industry. The article gives a thorough description of issues related to technological developments in the raw materials sector, oil refining industry, development of integrated and advanced mineral processing systems, and the use of household and industrial wastes. The research presents basic technology contributing to sustainable development, starting from exploration and production forecasting and up to sustainable planning and distribution of material and energy resources based on real-time data. It also pays special attention to the possibilities of creating digital platforms for the mineral sector. Digital integration, combining research areas, personnel, processes, users, and data will create conditions for scientific and technological achievements and breakthroughs, providing scientific and economic developments in related industries and, above all, in the global mineral and raw materials market.

Introduction

The mineral industry comprises a wide range of enterprises, from artisanal, low technology, informal operations to large-scale multinational enterprises using state-of-the-art technologies to extract and process minerals. Minerals, including fuels of mineral origin, are essential resources for societal development (Sverdrup et al. 2013). The mineral industry has several main segments:

the mining, processing, and metallurgy of iron and ferro-alloy metals;

the mining, processing, and metallurgy of nonferrous metals;

the mining, processing, and metallurgy of precious metals;

the mining and processing of industrials;

the mining and processing of construction minerals;

the mining and processing of precious minerals; and

the mining and processing of minerals fuels.

The minerals industries comprise numerous different, highly specialized activities such as: exploration; mining engineering; environmental and social assessments and management; minerals extraction, hauling, processing; metallurgy and metals refining, finance, legal management, marketing. The mineral sector of the economy is a combination of industries engaged in the extraction and primary processing of minerals, the explored reserves of which create the mineral resource base. The limitations imposed by the mineral sector have a significant impact on the overall challenges facing the world community. Consumer requirements for the quantity, quality, and velocity of supplying minerals, metals and energy create the need, and thus opportunities for industry renewal and efficiency improvement.

According to BP Global (Statistical Review of World Energy 2019), about 85% of the world’s energy comes from fossil fuels. For the foreseeable future, the mineral and raw materials sector of different regions and countries must deal with the issues of ensuring energy, minerals and metals supply security and become the guarantor of “sustainable development,” which is the basis for meeting the needs of future generations (Calvo et al. 2016; ICMM 2016). Several studies question the longevity of world’s fossil fuel and/or mineral resources and reserves and suggest that someday mining operations will reach maximum production rate and begin to decline if the industrial world does not develop new technological solutions (Höök et al. 2012). The development of technology in the mineral resource sector, the support of high-tech companies, the provision of a favorable environment for start-up projects, and the rapid introduction and commercialization of new developments are prerequisite factors for creating a competitive economy of any country. However, the cost of mining projects implementation reaches several billion dollars. However, the capital investment (CAPEX, for capital expenditure) needed to start new large-scale mining operations can reach billions of $US. On average, the CAPEX of mining projects documented by public feasibility studies is about 500 M$. However, for projects likely to have a significant impact on the production of main commodities such as Al, Cu, Fe, Ni, and Zn, the CAPEX requirements are frequently in the Bn $US range, especially if the project includes building one or several smelter(s) and refinery(ies) and/or large-scale transport infrastructures such as railroads and/or deep-sea harbors.

On average, the payback period for projects is 3–12 years, for areas with lack of infrastructure and remoteness from large centers, the period reaches 15–35 years, and it can reach up to 50 years for the development of the Arctic with low-cost hydrocarbons. At the same time, mining and geological risks are substantial, and demand markets cyclically change (Toxicol 2008). Concurrently, in view of the high capital intensity of mining projects and the need to control operating costs and to further improve the overall efficiency of the mining industry, there is much scope for further automation of production processes, especially in remote areas/challenging environments such as the Far North; landlocked areas or areas with scarce energy and water resources, or in the development of offshore fields (Benndorf and Jansen 2017). Therefore, only very powerful companies can take on technical and financial risks for carrying out such projects, and they even try to cooperate to reduce risks during the implementation of large-scale projects. Given this, the decision-making process for the development of the mineral resource complex needs more information and knowledge. Planning the use of natural resources at all scales requires new consistent methods to assess the impact of mining and resources utilization, and especially requires the introduction of sophisticated technological solutions that will provide reliable and unbiased results (Haines et al. 2013).

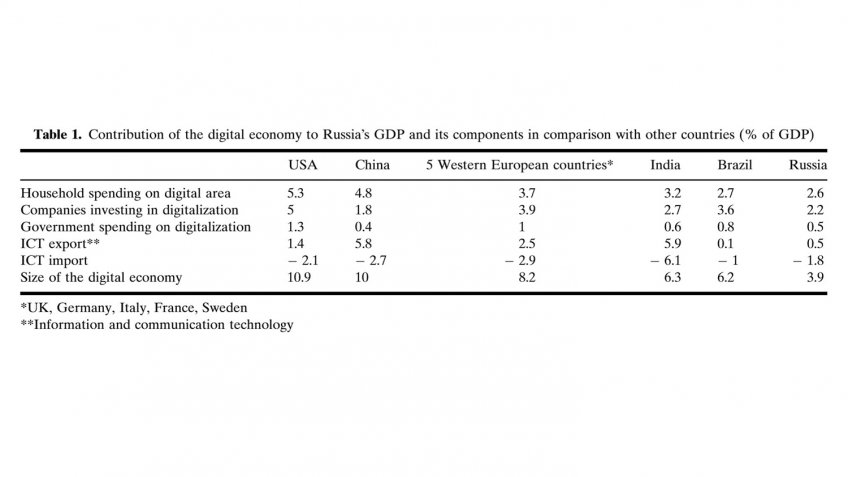

In this regard, the question arises: what should the mineral resource complex expect from the digital economy? The digital economy is not just a separate sector, but a system of economic and social relations based on the use of digital technology, the penetration of which in the near future will unite the real and virtual world, which in turn will qualitatively transform the economy and energy markets (Zhukovskiy et al. 2019a, b). Global socio-economic trends are accompanied by rapid technological changes, which lead to a sharp increase in the types and quantity of mineral products used in sophisticated technology and applications (Christmann 2018). Digital transformations are one of the main factors of global economic growth (Table 1). According to the research of the McKinsey Global Institute, in China, the GDP increase up to 22% by 2025 may occur due to Internet-based technology. The advance of scientific and technological progress and the disappearance of certain activities due to the penetration of automation increasingly supported by artificial intelligence, the Internet of Things, nanotechnologies, and 3D printing, into all stages of production processes are the factors of possible growth for enterprises of the future. Studies have shown that the existing workforce capacity of the mining industry is hardly able to promote digital transformation, and even can hinder it in many ways (Kazanin et al. 2014; Tao et al. 2018). In addition, new skills must be developed on an international level to ensure sustainability management for all countries (Global CIO Survey 2017–2018). In the USA, the expected increase in the value created by digital technology is not less impressive—it can reach 1.6–2.2 trillion dollars by 2025. The potential economic effect from the digitization of the Russian economy will increase the country’s GDP by 4.1–8.9 trillion rubles (measured in 2015 rubles), which amounts to 19–34% of the total expected GDP growth (Medvedev 2018; McKinsey and Company 2019).

Table 1 Contribution of the digital economy to Russia’s GDP and its components in comparison with other countries (% of GDP)

- *UK, Germany, Italy, France, Sweden

- **Information and communication technology

In the mineral resource sector, technology determines the future of the global commodity market while being one of the most difficult areas to predict. Providing a reliable assessment of the risks associated with the supply is necessary to support each country’s own interests in the field of economics and national security. It is almost impossible to conduct a risk assessment of an offer without information on the production and consumption of mineral raw materials in each country. Since the demand and supply of mineral resources are dynamic quantities, their analysis should also be dynamic (Fortier et al. 2018). The dawning of the fourth industrial revolution leads to very considerable uncertainties about the success of various technological areas (Zhukovskiy et al. 2019a, b). This issue is relevant since many important challenges facing society are related to the availability, development and use of natural resources. The assessment of the availability of energy and mineral sources and a high level of the technological component will help to make informed decisions regarding these resources (Fortier et al. 2018). Information about minerals, such as dependence on imports, production concentration in the country, growth in world production, price volatility, and global (world) management, are all important data for assessing the risks associated with the supply of basic, critical, and strategic minerals and materials. More detailed information about minerals, for example, for individual rare-earth elements, trade flows of various minerals and a wider part of the supply chain of mineral products (concentrates, metals, oxides, etc.) is needed to provide a more complete picture of the risks.

Main Straight-Through Digital Technology

The Industry 4.0 program uses the capabilities of the so-called “Internet of Things” (IoT) and the Cyber-Physical System (CPS) in the industry and production processes, which is associated with the acceleration of digital technology development and the gradual depletion of the growth potential and efficiency of traditional industrial, economic and social systems (Berman 2012; Thoben et al. 2017). The development and penetration of digital technology in all engineering and social strata produce global changes that will inevitably affect the mineral and raw materials sector and the technological sphere, triggering an extraordinary growth of some technologies (e.g., blockchain, DPS and BIM technologies, intelligent sensors, digital twins), the need for system integration, the seamlessness of this integration, and the system masses and fading interest in outsider technologies (e.g., Scada systems, ERP, and MES systems).

The mining industry has recently moved to digitalization of the supply chain and the introduction of blockchain technology (Deloitte Tech Trends 2019). Herewith, the abundance of natural resources and lower labor costs cease to be the main growth promoting factors; the development drivers will come from social and technological innovation, with digital transformation based on straight-through technology (Katuntsov et al. 2017). It is true with the mining enterprises, their efficiency greatly depends on the impact of hardly predictable policy, regulatory, economic, environmental, social, governance, technical and geological factors. The main “straight-through” digital technology include the following: “big data,” neuro-technology, artificial intelligence, distributed ledger systems (blockchain), quantum technology, nanotechnologies, powder metallurgy and 3D printing, industrial Internet of things, robotics and sensor technology, “cloud technology,” virtual and augmented reality technology, and digital modeling (Bahga and Madisetti 2016; Makhovikov et al. 2019).

The Industry 4.0 program provides for the straight-through digitalization of all physical assets and their integration into the digital ecosystem together with partners involved in the value-added chain. Cyber-physical integration is an important prerequisite for smart manufacturing. Digital technology allows the introduction of network interaction between machines, equipment, buildings, and information systems (Zhukovskiy and Malov 2018). “Things” monitor and analyze the environment, the production process and their state in real time. In addition, the transfer of control and decision-making functions to intelligent systems and algorithms lead to a change in the paradigm of technological development of enterprises. Cyber-physical systems (CPS) and digital twins (DTs) are the preferred means of such integration. CPS are multi-dimensional and complex systems that unite the cyber world and the dynamic physical world. DTs are a software analogue of a physical device or process that models the behavior of a physical object under the influence of interference and disturbances, as well as the environment and the human factor. Cyber-physical integration and real-time interaction is achieved in order to monitor and control physical objects in a reliable, secure, collaborative, reliable, and efficient way. DT creates high-quality virtual models of physical objects in virtual space to simulate their behavior in the real world and provide feedback. As the preferred means of cyber-physical integration, CPS and DTs pave the way for intelligent manufacturing, which would fundamentally transform existing production systems and business models.

Basic Conditions of Digital Technology Development

The efficiency of commodity markets development in the digital economy is possible only with the availability of advanced technology. It is efficient to create a model of technological development based on the principles and methods of cognition (Latin Cognito—comprehension, knowing, awareness). The IoT paradigm is extremely susceptible and adaptive to new principles and architectures related to various areas of science and technology (Liu et al. 2017). The minerals and metals industry of the global economy is high-tech and knowledge-intensive, and so the main directions for the implementation of digital technology should focus primarily on two basic conditions.

Firstly, the organization of research and educational centers (RECs) require the development of the applied digital economy (i.e., organizational and policy management, personnel, the system of professional knowledge assessment, new professional standards, and educational systems with the improved scientific support of training) and observance of the following conditions:

improvement of equipment, technology, and technological processes through the introduction of well-known and new scientific knowledge (evolutionary and revolutionary scientific and technical progress);

unrestricted access to information (receiving, transmitting, and exchanging data);

updating the list of highly demanded professions, due to the intellectualization, digitalization, and automation of work processes; and

job retraining and training of new specialists.

Secondly, the development of main infrastructure elements of industry-specific digital technology—information and computing infrastructure, information security. The REC in the process of digital technology development (Fig. 1) is a basic block of network interaction, and several RECs form a node. Combination of nodes creates a sectoral cognitive cluster REC. Cognition means that the combination has the following general properties:

the ability to self-analyze and reconfigure based on the existing environment, demand, current goals resulting from assigned tasks;

the ability to adapt its state according to the existing conditions or events, based on certain criteria and knowledge of previous states and accumulated experience;

the ability to dynamically change its topology and/or parameters by the requirements of technological and social challenges;

the self-configuration with distributed control based on rules and established management mode; and

the possibility of self-determination of its current state and usage of this information for planning of its work including making certain decisions as feedback to the current situation and demand.

The international competence centers connect regional cognitive nodes or clusters of international nodes; they also play an integrative role in the dissemination of knowledge and technology outside the region and country. The proposed structure enables development of research competencies and technological base for the efficient introduction of digital technology in the entire technological chain of all mining operations (prospecting, exploration, production, transportation, processing, and obtaining a direct consumption product).

Establishment of Research-Education Centers

Global changes in management remain the weakest side of the introduction of digitalization in Russian and foreign enterprises. The digital age is moving at such a rapid pace that it is mainly challenging organizations in both the private and public sector, as it requires new ways of thinking. Hence, this process greatly changes the functions of human resources departments (HR) in these organizations and their role in finding new approaches for managing people.

The result of the digital transformation of the economy is the key changes included in the framework of the “Industry 4.0” concept and “Industrial Internet of Things” (IIoT), which determine the world trend of scientific and technological progress: speed, flexibility, quality, and efficiency. The bases of this transformation are human competencies and skills. In the coming decades, the digitization will lead to a significant replacement of human labor with machines and the release of a substantial share of the labor force, which will create certain difficulties for companies and the state (Cascio 2019). Even in the largest international companies that are actively introducing digital technology, there are problems with highly qualified employees.

According to Logicalis’s Global CIO Survey 2017–2018 report, managers believe that barriers to digital transformation are outdated infrastructure (44% of respondents), unavailability of employees to adopt a new organizational culture (56%), and the cost of deploying digital processes (50%). Other problems include lack of proper technical skills (34%), security problems (32%), and lack of interest in transformation (11%). In addition, the search for qualified personnel today has become a real problem due to the lack of knowledge and skills in the appropriate volume on automation and digitalization of the business in the mineral sector. Therefore, in the Russian context, most of the projects for introducing IT systems today are aimed at automating, rather than at transforming business. These systems store a huge amount of data about what is happening in production, but the level of their analytics remains weak. It is necessary to use the opportunities that technology gives us in order to obtain, perhaps, fundamentally different business models, changes in the characteristics of the organization’s work itself, and business procedures. This transformation includes changes in thinking, leadership style, the system of encouraging innovation, and in adopting new business models to improve the work of the organization’s employees, its customers, suppliers, and partners. A more difficult stage in the transformation of the company is the restructuring of all the processes of the organization, the development of staff competencies, and the creation of confidence in new digital technologies.

According to a survey out of thousand persons surveyed, 31% reported that, after 6 months, they left for a new job due to the lack of readiness for change. This survey was conducted for employees of mining companies in Russia who took additional education courses at St. Petersburg Mining University. The total number of respondents was one thousand people from 19 companies who are engaged in the mining and processing of coal, ore and building materials. By 2020, up to one-third (about 50 million people) of the US workplaces can be modified (The changing role of people management in the digital age 2016). The issue of motivation and training of personnel is of paramount importance. It is necessary to improve the education system that will provide the digital economy with competent personnel (Richardson and Bissell 2019). At least 57 professions will disappear, but 187 new ones will be created in Russia (Atlas of emerging jobs 2019).

The term “the half-disintegration of competencies” is used to assess the rate of obsolescence of specialist knowledge, meaning the length of time after graduation, when, due to the emergence of new scientific and technical information, the graduate’s competence decreases by 50%. Today, the half-disintegration of knowledge in the field of science is about 5 years. It is necessary to increase the competence of specialists in the field of digital technologies in the framework of existing domestic and international training programs (World Bank 2018).

The training of new personnel ready to work in digital mineral resource technologies, should have already been started “yesterday,” since the scientific and technological process in the mineral resource sector is gaining tremendous momentum, the half-disintegration of competencies in this industry will almost catch up with the IT sector development by 2030 and will equal to 2–3 years. At the same time, digitalization should occur synchronously with the modernization of the laboratory facilities and the knowledge of teaching staff in universities.

Currently, the scientific and industrial community, not only in Europe but also in the whole world, actively discusses what skills engineers and bachelors should have within the current trend of the fourth industrial revolution of “Industry 4.0” and the pervasive Internet (Gruber 2019). It is obvious that the main skill of a person should include the most demanding characteristics of the future, i.e., flexibility, since the speed of changes is significant. Therefore, this property is highlighted as the main one, because it is very important to quickly respond, rebuild yourself, your competencies, learn new professions, and be always in training. A future professional is a person who can quickly adapt himself, his knowledge, and competencies to the rapidly changing technological world of networked multi-cultural collaborations. The training of highly qualified personnel based on modern technology and approaches to training will enable future industry professionals to quickly navigate themselves in the fast, massive, and fragmented information flow. Being flexible, adaptable to diverse work environments and open to technological change mean being in demand on the market of future professions.

Worldwide, the mining industry is confronted with multi-dimensional, frequently interlinked issues with sometimes very complex combinations of technical, economic, environmental, governance, and social factors. High-quality training of future mines and metal industry managers need to address all these factors. One of the main problems of creating high-quality training in the mining industry is the adjustment of knowledge to rapidly changing technology. In the next 20 years, the most demanded technological areas in the mining industry will be the following ones: additive production and powder metallurgy; artificial intelligence and big analysis, blockchain technologies, collective intelligence, data cybersecurity; industrial ecology, materials science; process control and automation, simulation and “digital twins”; “connected” transport; energy storage units; software packages and systems; communication and peripherals; automation.

When implementing educational and research programs, as well as advanced training of specialists, it is necessary to improve the quality of education. Figure 1 shows the network essential for the establishment of an innovative training system using adaptive training programs based on the most relevant inter-disciplinary issues. The competencies for straight-through technology should have special attention.

Russian objective is that, by 2024, the number alumni of higher education institutions related to information and telecommunication technology should reach 120 thousand people per year. In 2016–2018 research (supported by several questionnaires) on mid-ranking mining specialists in the areas of automation, energy, mechanization, and economics was conducted. This study was conducted for employees of mining companies in Russia who took additional education courses at St. Petersburg Mining University. The total number of respondents was 645 people from 19 companies who are engaged in the extraction and processing of coal, ore and building materials. Of these, the number of experts in the field of automation was 165 people, with ages from 32 to 54 years. The number of power engineers and electricians was 170 people, with ages from 28 to 52 years. There were 160 people from the mechanization, with ages from 28 to 54 years, and 150 people from the economy industry, with ages from 33 to 48 years. The questionnaire had 30 questions; it was used at the hiring stage to assess the level of competence in the target technology on a maximum scale of 5 points. Figure 2 shows the averaged data (for 2 years) for specialists of four sectors.

The survey showed that, in almost all areas of competence, the specialists did not reach the average level, and in some areas, the specialists of all sectors failed. There is an urgent need to adjust training programs, accelerate the development of competencies, and stimulate this process to ensure the development of the mines and metals industry. The survey also proved the need for a specialist to combine the skills of several professions. If we assess the level of competence of specialists from different sectors of the mining industry, it is obvious that the level of competence in 8 out of 14 technologies is above average. It proves that a future specialist needs to have versatile knowledge and be flexible to master related and additional specialties.

However, currently, engineers and economists have, as presented in the study, the lowest scores for the majority of digital technology trends. Considering that, in the future, the Industry 4.0 will penetrate deeper and deeper into the field of engineering, energy, and economics, specialists with digital competencies for the mining industry will be in demand in the next 10 years, and beyond. As a result, we should expect the demand for specialists having competence in these areas; therefore, interaction with educational partners to create new educational programs is vital for mineral resource companies.

Information Infrastructure

It is impossible to meet the needs of society, business, and government without the development of communication networks, data center systems, and the introduction of digital data processing platforms.

Modern enterprises need an IT infrastructure consisting of an integrated set of systems, programs, and services to ensure efficient operation. With digital changes, technological tools come into quickly and easily measure and test the solutions. The IT infrastructure must be complete, highly reliable, well-designed, have a large margin of safety, and match not only the current state of the business but also consider future development trends (EIA 2018).

The issue of infrastructure development is one of the fundamental objectives of the UN Department of Sustainable Development. It states that by 2030, international cooperation needs to be expanded to facilitate access to research and technology in the field of clean energy, including renewable energy, energy efficiency and advanced and cleaner technology using fossil fuels, as well as to encourage investment in energy infrastructure and technology of the mineral resource sector (Goodenough et al. 2018).

According to the Global Infrastructure Hub, it is necessary to invest up to 307 billion dollars in the information and telecommunication infrastructure. Today’s investments in the five selected regions are estimated at only 277 billion dollars (Global Infrastructure outlook 2019). The largest investment gap is in Asian countries—15 billion dollars. (Fig. 3).

Investments in information infrastructure in the world 2019–2030

Information Security

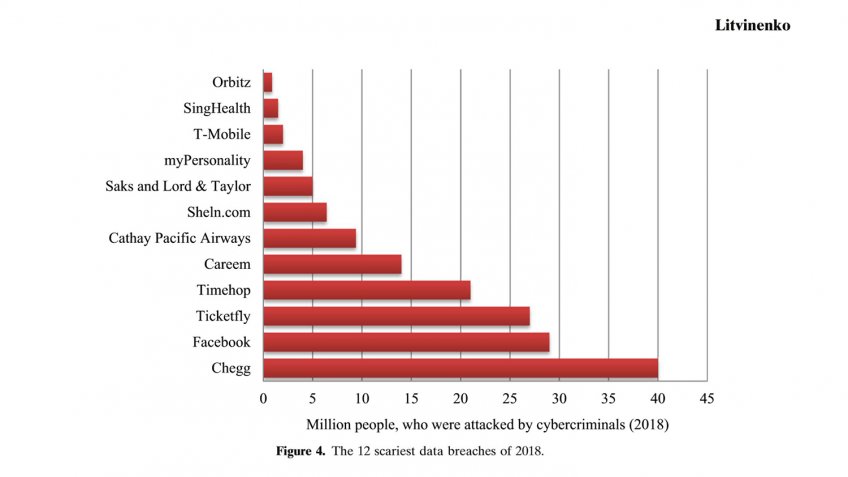

Industry specialists suggest that information security means the stable state of information protection, its carriers, and infrastructure, which ensures the integrity and stability of information-related processes to intentional or unintended natural and artificial impacts. Impacts are information security threats that can harm the subjects of information relations. Information security is an important aspect not only for the mineral sector but also for the digital revolution as a whole. For example, companies like Facebook and Google, which, at first glance, have already reached digital maturity, are under attack from hackers. This is of great concern to the mining industry too. According to Kaspersky Lab for 2019, in the USA alone, 163 million user records have been hacked this year (according to data provided by the Resource Center for Personal Data Theft). Some of the biggest companies attacked in 2018 include T-Mobile, Google, Orbitz, and Facebook (Fig. 4).

The 12 scariest data breaches of 2018

It is necessary to increase the number of citizens competent in the field of information security, media consumption, and the use of Internet services. It will enable protection of an individual, the society, and the state from internal and external data breaches and ensure the realization of constitutional rights and freedoms of a person and a citizen, decent quality and standard of living of citizens, sovereignty and sustainable socio-economic development of all countries. It is also necessary to pay more attention to studying the information security in universities; classes should include real-life cases—lessons, tests, and simulations that will help employees and students to assimilate large amounts of information and integrate their knowledge into daily work, creating the basis for a culture of cybersecurity.

Organizational and Technological Priorities in the Mineral Sector of Russia

The use of digital technology in the development of mineral deposits will require not only significant technological changes but also organizational and even behavioral changes. Management structures will undergo a slow renewal, and the role of deep analysis in the adoption and implementation of complex decisions will take on greater significance. The key challenge presented by the digital transformation lies not in determining the appropriateness of digital solutions, but instead in the underdeveloped state of digital culture and the shortage of digital technology specialists within companies. It is vital to create proper conditions for training a new kind of employee, skilled in new technologies, and capable of adapting to digital realities. Within the framework of the Russian program “Digital Economy,” a competence center was established by dozens of Russian companies. However, considering the specifics of mining or oil and gas enterprises, it is necessary to use industry specificity and cognition (Fig. 1) to spread digital technology to transform the industry and increase the efficiency of the entire mineral and raw materials sector.

In the context of global inter-sectoral and inter-disciplinary integration, practical digital technologies will directly affect the economic and technological development of mineral exploration, extraction, and processing, transportation, and use of minerals. It will shape significant geographical and structural shifts in global markets for minerals and products derived from mineral processing.

Countries possessing unequaled mineral potential have not only a unique chance to improve efficiency in this sector, but also extensive emerging opportunities to improve labor productivity in the industry. Key preconditions for this are the adoption and implementation of organizational and legislative solutions in parallel with digital technology in the following areas:

- Measures to save energy and reduce metal consumption throughout the national economy. Data on energy resource loss indicate that the Russian economy loses approximately 400–420 million tonnes of oil equivalent annually on the journey from extraction to the end user. It includes losses in the housing sector and manufacturing, but the greatest losses occur in the fuel and energy industry itself (Abramovich and Sychev 2016). Thirty percent of these losses are associated with the lack of a modern organizational and legislative mechanism for managing the process. The establishment of an integrated system throughout Russia, based on information and communications infrastructure for managing the consumption of energy resources, could have a huge annual effect on the economy (Steininger 2019; Wood et al. 2019).

- Deep integration and intellectualization of energy supply systems. Separate in the management and legislation areas the systems of electricity, heat, cold, and gas supply using digital solutions should form a “System of Systems” (SoS). As part of solving the problems of growing demand for electricity and physical deterioration of networks, the birth of the “Smart Grid” concept was natural. However, the digital change transition only will not suffice for the transition to a new technological order. Smart technologies and integration are needed for all components of the energy industry such as generation, transformation, transportation, and, even more essentially, in the uses of energy. It also will allow the integration of electricity, heat, cold, and gas supply systems. The digital network would allow monitoring and controlling parts of the system at higher resolutions in time and space. One of the goals of an intelligent network is to exchange information in real time in order to make work as efficient as possible in terms of unit costs for the production, transmission, and consumption of all types of energy.

Energy requirements are constantly changing, and it will inevitably require greater integration of energy into the technosphere. There are tight requirements for efficiency, energy security, environmental friendliness, energy efficiency, and adaptability of the energy infrastructure. Increasing the utilization of energy resources at the stages of generation, transportation, and final transformation should be effectively and closely monitored (Plewnia 2019).

- Problems connected with the use of associated petroleum gas (APG). The volume of gas is directly dependent on oil extraction. The rate of petroleum gas use lags significantly behind the rate at which it is being extracted, leading to steady growth in volumes of combustible gas at flare plants. The use of APG, which possesses unique properties, can be broken down as follows: around 25% is burnt off at flares and disperses into the atmosphere, around 45% is used for industrial purposes and consumed in process losses, and only around 30% goes on to be processed. Issues relating to the utilization of petroleum gas are of a complex, multi-sectoral nature, and it will be some years before an optimal solution can be found. Losses are very significant; according to the most optimistic estimates, more than 20 billion cubic meters of APG are burnt off annually. For Russia, the full use of associated petroleum gas would mean annual production of 5–6 million tons of liquid hydrocarbons, 3–4 billion m3 of ethane, 15–20 billion m3 of dry gas, or 60–70 thousand GWh of electricity. It is essential to implement digital technologies, which will enable a state monitoring system, and to establish increased environmental fines as an incentive for subsurface users, together with more stringent licensing requirements (Messmann et al. 2019).

- Comprehensiveness and completeness of prospected reserve development. These issues are associated with the lack of unified state digital technologies for monitoring extraction and the proper functioning of extraction equipment at each well and subsurface facility. For example, the average percentage of oil recovered nationally is 28–33%, which is almost half the ratio cited by leading oil companies. It can be said with a comparatively high degree of certainty that Russia’s oil reserves are primarily made up of deposits that have already been developed. These are deposits with a developed infrastructure, and the effect of increasing recovery by just 1% across the country could translate into a value of around USD 5 billion annually. The delineation of responsibility between the state and subsurface users has become blurred, and this is detrimental to reserve recovery and expansion of the minerals base (Shmal et al. 2019). Legislative mechanisms and state oversight of digital technology across the full development process for explored reserves are currently lacking.

- Addressing issues in the development of new approaches to the regulatory and methodological evaluation of reserves and resources. It is essential to make use of new methods for evaluating reserves and resources to ensure that the development of strategic programs and energy sector growth forecasts are well-founded, to unveil the investment attractiveness of the Russian fuel and energy industry’s minerals base, and to stimulate innovative development. We can formulate a three-dimensional model for classifying hydrocarbon resources:

Geological knowledge and accuracy

The economic significance of reserves

The technological and economic underpinning of extraction technologies and opportunities for complete recovery of hydrocarbons and associated components from the subsurface

Besides the listed, it is suggested to add social and environmental impacts to this list, as well as their mitigation measures. There is a huge need for such an evaluation, based on three-dimensional digital models for classifying resources, primarily among oil companies operating offshore, as it will enable them to obtain a more objective view of prospective opportunities to develop their hydrocarbons base and its extraction potential.

Considering global experience and prospects for addressing the problem in Russia, the level of scientific and technological progress achieved, and market conditions over the next 10–15 years, the oil recovery rate in Russia could increase from 30 to 60%, which corresponds to the Russian Federation’s real potential and extraction opportunities.

- Development and manufacture of equipment, as well as development of services, to support operations to increase oil recovery and utilize APG (Litvinenko 2019; Mukherjee and DebRoy 2019).

- Unique hydrocarbon potential of the Arctic Shelf is a special focus of government regulation. The operations of national public oil and gas companies in the Arctic are being hindered in many respects by the lack of a unified state center for coordinating the activity of all participants working to create a fleet of icebreakers, shipping ports, airports to facilitate offshore exploration and extraction, and LNG facilities. A unified coordination center equipped with digital technology for determining the project’s implementation status in real time could ensure effective organization of Arctic development, making practical use of the available transport system and fully realizing the mineral potential of the Arctic Shelf. Currently, Russia is developing the newest innovative surveillance and communication system in the Arctic zone of the Russian Federation—the multi-purpose space system (MPSS) “Arktika.” The integration of the data received by the system with the already functioning and advanced observation and monitoring systems will not only improve the quality of navigation systems throughout the Northern Sea Route but also reduce the risk of emergencies.

The above are only some of the current issues that require both the implementation of digital technology and the improvement of state regulation of working processes at deposits and relationships between the state and subsurface users.

Challenges and Technological Opportunities in the Mineral Sector for the Period Till 2040

A rapidly growing population (set to reach 9 billion by 2040, according to UN estimates) and economic growth in developing countries are leading to clear geographical and structural shifts in global mineral and mineral product markets (World energy council 2019; World Bank 2018; EES EAEC-private 2019). Thus, over the past 25 years, rapid economic development, especially in China, has led to an increase in the standard of living of hundreds of millions of people around the world. Projections of recent growth and development trends suggest that there are still 3 billion people worldwide can reach the living standard of the middle class (measured by purchasing power parity) between 2009 and 2030 (Kharas and Gertz 2010).

According to estimates by international energy agencies, oil extraction growth was concentrated in only nine oil-producing countries, growth in natural gas production in ten countries, and coal production growth is possible only in four countries, while the rest of the world as a whole has passed the peak of production for these resources (Table 2). It is obvious that after 2030 the natural gas and oil market will be almost monopolized by four or five countries. The challenge is the transition to a completely different energy paradigm to protect the world from the threat of a scenario of possible price manipulation. However, the most important threat is the ecological situation in the world is climate change, global warming, with evaporation of methane stored in the permafrost as one of its powerful drivers. Today it is perceived as a potentially very powerful factor in the use of completely new methods and approaches.

Coal is becoming to play a key role in Russia, and therefore, the transition to ecological and efficient technology for processing coal comes to the fore (Litvinenko and Meyer 2017; Meyer et al. 2018).

Wide-ranging opportunities to increase labor productivity in mineral prospecting, exploration, and extraction are already available through geographical information technology. The development of remote sensing and global positioning (navigation) systems makes it possible to use information and communications infrastructure to create integrated systems for managing the processes involved in prospecting, exploring, extracting, and transporting minerals (Spulber 2019).

The development of biotechnologies influences the structure of long-term demand on extractive industries and promotes the restoration of ecosystems through bioremediation of soils and seafloors polluted by hydrocarbons. It also offers solutions for more efficient mineral processing and recycling of metals from urban waste. The volume of the global biotechnology market today is estimated at 270 billion dollars, and the projected growth rate is 10–12% per year until 2020. Based on the findings from Frost and Sullivan 2014, it is expected that the market will amount to about $600 billion in 2020. The companies of two biotechnology centers—the USA and Europe—earned more than $133 billion in 2015, and this value will exceed $220 billion by 2017. According to the forecast of the OECD and the Food and Agriculture Organization of the United Nations (FAO), by 2022 the volume of bioethanol production will increase to 168 billion liters, and biodiesel to 41 billion liters. The main driver of market growth is the state policy of encouraging the use of fuel sources from renewable raw materials (International Renewable Rnergy Agency 2019). The main pursued goals are to reduce dependence on traditional energy sources and to improve the environmental performance of transport (Annual statistics of world energy 2018). The emergence of new materials based on nanotechnology is changing the structure of demand for materials. It is increasing for some thinly dispersed (quite widely available in the Earth crust but rarely form economic concentrations) rare-earth elements (Kathryn et al. 2017; Goodenough et al. 2018; Jiang et al. 2018).

As the digital economy develops, the global minerals market is anticipating the challenges mentioned in the following sections.

Global Reduction in the Specific Return on Investment in Geological Exploration

Global investment in geological exploration is worth billions of $ US annually. The range was 7–21 bn$ US/year during the current decade, according to annual reviews published successively by Metals Economic Group, SNL and now S&P, on occasion of the annual Prospectors and Developers Association of Canada (PDAC) Convention. Volumes extracted by international companies are outstripping the volume of reserve growth by 5–20% (Meinert et al. 2016; McKinsey and Company 2016). Easily accessible reserves with a high useful mineral content are being exhausted especially quickly. The investment direction in the geological exploration of metals deposits greatly varies and depends on the country: Although in the most countries, the primary investment is in gold, in Eurasia the primary investment is in copper, nickel, and other nonferrous and rare-earth metals. In Russia, over the 40 years the average metal content of nonferrous metals ores has more than halved. The metal content of ores in the newly placed under production deposits has fallen: for lead, from 6 to 1.3%; for gold, from 15 to 1.5%; for nickel, from 4 to 0.4%; and for copper, from 1.5 to 1% (Nornikel 2017).

Improvement in Technology Used in Geological Exploration

Active usage of remote sensing technology reduces labor costs and minimizes the impact on the biosphere (Litvinenko 2019). Science-intensive technologies for geophysical research are developing at a fast pace, including nuclear, geophysical, and seismo-acoustic, deep geo-electrical engineering, geodetic gravimetry, geothermal, and geo-electrical prospecting. Geological exploration widely uses small drones (American Association of Petroleum Geologists 2018).

Geological Exploration for Uranium

In general, world uranium mining has not yet reached its peak; in 2017, the mining volumes fell as compared to the record year 2016, but the trend is still positive. Within 40–50 years, the world will have exhausted its reserves of uranium-235 (World Nuclear Accociation 2018; International Atomic Energy Agency 2018).

Depletion of Traditional Hydrocarbon Reserves

Any changes lead to the emergence of new needs on a global or regional scale and the introduction of new technology to meet them. It promotes an increase in the volume and acceleration of energy consumption per unit of time. In the future, the growth of new energy systems will ensure the safe energy supply when fossil fuels begin to become increasingly scarce; today it is necessary to minimize their negative impact on the environment (Pashke 2017; PwC. Mine 2018).

Major explored deposits are in hard-to-access locations. They are distinguished by the high resource and energy costs associated with developing them and the need to build infrastructure to do so. Oil is presently extracted at a considerable energy cost: Whereas 30 years ago, the energy represented by one barrel of oil was sufficient to extract 100 barrels or more, today an average of one barrel is needed to extract just ten barrels, and the amount of energy required is continuing to grow rapidly. This ratio may reach 1:1 within the next 30–50 years, rendering the industry non-viable. As problems associated with the exhaustion of traditional oil reserves intensify, interest in non-traditional oil is growing (Ernst and Young 2013): heavy crude oil, oil sands, oil shale.

Potential of the Arctic

According to data from the United States Geological Survey for 2014, unexplored reserves of traditional hydrocarbons in the Arctic total approximately 90 billion barrels (13 billion tonnes) of oil, 44 billion barrels (6.5 billion tonnes) of gas condensate, and 1669 trillion cubic feet (47 trillion m3) of natural gas. It represents approximately 13% of the total volume of the world’s unexplored oil reserves, 30% of its total unexplored natural gas reserves, and 20% of global gas condensate reserves (Central Dispatching Office of the Fuel and Energy Complex of Russia 2018). Large-scale development of hydrocarbon deposits in the Arctic zone will require the implementation of effective environmentally friendly technology, the development of which will necessitate significant investment. It is also essential to develop comprehensive measures for repairing the damage that may be caused by accidents. There are grave risks associated with climate change, which could lead to the destruction of extractive industry assets in the Arctic as well as environmental disasters.

The role of digital technology in the energy sector and the development of the Arctic would reduce potential threats of accidents. The reduction in black carbon, methane, and tropospheric ozone can immediately reduce the Arctic warming to 2/3 (Shindell et al. 2012). Thus, digitization of production, clean coal technology, and CO2 capture technology from the atmosphere would significantly reduce environmental pollution and, as a result, slow down the melting of ice (Above the Arctic: an intel drone expedition 2019). Artificial intelligence technologies could help determine the rate of ice melting, climate change, and flow directions. It would be able to determine the impact of human actions. The fragility of the Arctic ecosystems implies that measures to preserve the unique flora, fauna, and landscape should be foreseen during the development of the subsoil. Measures include the creation of ecological corridors for the migration of wild animals, the reduction of noise during shipping, as well as the support of local people whose traditional lifestyle would inevitably change in the future. It is required to prepare a methodology for monitoring the level of environmental pollution and climate change, which would allow assessing the damage and control the implementation of environmental legislation requirements. Digital technologies would be able to improve thermal stabilization systems to preserve permafrost, as well as increase the observability of dynamic heat distribution processes. The ecological ecosystem of this region is unique and fragile, so the development of resources using the best technologies is relevant.

Development of Systems for Deep and Comprehensive Mineral Processing

Contemporary research in minerals processing aims to improve the environmental economic and energy efficiency of technological processes, as energy and water requirements are very important in rock grinding and flotation processes (Dagasan et al. 2019). Work is being carried out to replace environmentally hazardous extraction and enrichment technologies with cleaner alternatives. Another important trend is the transition to the maximum fineness of separation (dispersion), which is making it possible to achieve fuller recovery of useful components from ore, newly developed crushing systems capable of processing ore to the micrometer level making this possible. The implementation of new processing technologies is leading to a 15–20% reduction in unit water consumption and a 30–50% reduction in unit electricity and reagent consumption. It is anticipated that productivity at processing and enrichment facilities will increase by 10–40% (Dagasan et al. 2019).

Growth in the Use of Mining Wastes

Extraction of useful components from the waste produced by mining operations is now becoming economically viable. Every year, the extraction and processing of useful minerals lead to the accumulation of 17.4 billion tonnes of solid and liquid waste globally, a large part of which is solid waste from mining operations. Many countries view man-made waste as an important component of their national economy’s resource base (Messmann et al. 2019).

Growth in the Use of Domestic Waste

In developed countries, and European countries especially, figures indicate a stable reduction in the material intensity of GDP (more than 1% annually) over the last two decades, as efficient industrial technologies, less material-intensive machines, and equipment designs are being introduced (OECD 2018). Waste recycling technology (in particular, smart sorting, plasma-assisted combustion, pyrolysis, and biodegradation) are improving, providing economic justification for the spread of waste recycling and reuse practices along with the development of a technological foundation and unique skills in this area. In the long term, it is possible to reduce the demand of the European Union countries for such types of raw materials as metals and wood and paper products. Different technological development trajectories affect the demand for various metals over time, as well as technological substitutes and the development of the economy. The role of recycling is also essential to meet demand. The European companies specializing in the development of anthropogenic mineral deposits will seek expansion, obtaining licenses for the development of large landfills and tailings in other countries around the world (Benndorf and Jansen 2017).

Development of Renewable Energy Technology

The share of energy produced from renewable resources in the European Union is now more than 13% and is continuing to grow (Enerdata 2018). Large-scale use of renewable energy sources is creating the need for additional energy storage systems, and “flexible” hydro and gas generation, capable of providing backup production when the conditions necessary for producing energy from renewable sources are not present. The development of solutions to improve the economic and technological efficiency of renewable generation is ongoing, with a particular focus on reducing the need for rare-earth metals in the production of generating equipment. However, the metal intensity of renewable energy sources in terms of 1 MW is significantly higher than that of non-renewable ones. In particular, it takes an average of 542.3 tons of steel (iron) to generate 1 MW of electricity using wind, while using natural gas for the same needs requires 5.3 tons per 1 MW (Månberger and Stenqvist 2018). Large-scale development in other technological areas (such as fuel cells powered by various kinds of fuel, etc.) is unlikely to occur before 2040 (Atomic Expert 2018).

Development of the “Smart Mine” Concept

The smart mine project, financed by the European Union, is aimed at developing technologies and expertise that will make it possible to construct automated underground mines that require minimal human presence and have limited environmental impact (SmartMine 2019). The key characteristics of a “smart mine” will include:

extremely high health and safety standards;

limited effect on the landscape;

low specific carbon dioxide emissions;

high level of recovery of the useful component from ores;

maximal use of remote processes, allowing a significant number of staff to be located in major cities with comfortable living conditions, rather than in the extraction zone;

storage of waste rock without removal to the surface, or the production of building materials and other useful products from waste rock; and

high energy efficiency.

Enhanced Oil Recovery Rate

Oil-extracting countries, both developed and developing, widely used methods of enhanced oil recovery, i.e., for increasing the share of a deposit’s reserves that have been extracted by the end of its development period (Krasnov et al. 2018). The USA, Russia, Canada, Venezuela, and Indonesia most widely use such methods. The major known technologies for enhanced oil require high costs, high levels of energy, and material intensity. They generally become cost-efficient at oil costs over USD 70 per barrel. Over the last decade, there has been a global expansion in the use of tertiary methods of increasing oil recovery, including thermal, gas, chemical, and microbiological methods. Thermal methods include thermal steam action, the initiation of intra-formational combustion, thermogas use, and the displacement of oil and asphaltenes with hot water. Gas methods include the action of hydrocarbon gas, carbon dioxide, nitrogen, and combustion gases on the formation. Chemical methods use displacement of oil with other substances, including surfactant solutions, polymers, thickening agents, foam systems, alkaline solutions, acids, and compositions of chemical reagents. Increases in oil recovery achieved using tertiary methods account for the extraction of an additional 110–130 million tonnes of oil equivalent annually worldwide (2.5% of global extraction). Existing hydrocarbon resources and APG, in particular, are being used increasingly efficiently. The leading countries for APG extraction and processing are Russia, the USA, Saudi Arabia, Canada, Mexico, the UAE (Abu Dhabi), Iran, Venezuela, and Algeria. Economically developed countries use up to 98% of APG. Over the last few years, the volume of this kind of fuel recovered in Russia has been increasing, yet the volume utilized for practical purposes remains unchanged, at a national average of 73– 78%. Currently, in Russia, APG is used primarily in the energy and petrochemicals sectors.

Growth of Environmental Risks

Experts estimate that 3–7% of oil extracted stays at oil fields; most of the pollutants (up to 75%) enter the atmosphere, 20% enter water sources, and 5% enter the soil (Murygina et al. 2014). In the context of global warming, the danger of oil polluting the seas is increasing due to reduced ice coverage, improved drift conditions for oil spills, and the increased likelihood of oil polluting the coastline. The hydrocarbon intensity of Russian GDP is significantly higher than in developed countries. As such, environmental innovations and other technology must be actively disseminated to reduce the burden on the environment. The waste recycling market is predicted to have high growth rates. The most sought-after technologies are those intended to reduce the resource intensity of production, to make full use of raw materials, and to prevent pollutants from negatively affecting the environment. Issues associated with reducing the burden on the environment and environmentally focused economic development (“green growth”) have become technological policy priorities in the leading countries of the world. According to Environmental indicator report by EEA (2018), the environmental innovation industry is now a significant sector of the economy, with an annual turnover estimated at EUR 290 billion, or approximately 2.06% of GDP (EEA 2018). Increased expenditure on environmental protection in tandem with the growth of per-capita GDP is a global trend. Currently, environmental protection measures use between 0.1 and 2% of global GDP, and in developed economies, this type of expenditure will reach 3–4% of GDP in the nearest future (McKinsey 2018). The adoption of stricter environmental standards, such as those associated with the use of the best available technologies, is resulting in increased production costs across some sectors. This market is expected to be worth hundreds of billions of dollars in the coming decade.

Digital Platforms for Mineral Resources

The challenges mentioned above limit the current development of the mineral sector and shaping its future progress. Technological capabilities can give a new boost, but the uncertainties related to the political decentralization in many parts of the world call for a technological breakthrough, a synergistic effect obtained through digital transformations (Hariharan et al. 2017; Juliani and Ellefmo 2018; Shubenkova et al. 2018). Technology and the social sphere can be managed and become efficient to become a guarantor of sustainable development (Ghassemzadeh and Charkhi 2016; Tessema 2017). Meeting the present needs requires finding a reliable, sustainable balance between the needs of all stakeholders, as shown for the example of the mining industry (Fig. 5). Due to the different specifics of the legislative bases of the regions, such as the USA, China, the EU, and Africa, the development of digital transformation is presented on the example of the Russian Federation. Balancing interests should occur automatically and be transparent. The creation of industry-specific digital platforms within countries will facilitate these radical changes.

The digital platform “mining industry” is a system of algorithmic mutually beneficial relationships of a significant number of independent participants in the mining industry, carried out in a single information environment. Smart contract technology will enable commercial agreements to be concluded and maintained through blockchain technology between three circuits: processes (including equipment), participants, and data (Christidis and Devetsikiotis 2016). Smart contracts can exist only within the digital platform environment; the executable code freely accesses the smart contract objects. Such an object can be a search for investment in geological exploration operations and the registration of summary data in bigger sectoral data (Beucher et al. 2015). This process uses the algorithm that checks whether a certain criterion for the specified conditions is met or failed and makes independent decisions based on the programmed conditions. Thus, the basic principle of a smart contract is the full automation and reliability of the execution of a treaty in all its parts.

Mining projects have many stakeholders; mining operations can imply significant risks for people, environment, and investment. Operational data can provide a basis for the use of artificial intelligence in the tasks of predicting the risks of violation of the conditions of safe mining (Aqil et al. 2007; Mokhtari and Behnia 2019). This appears true only if there is sufficient environmental and social baseline data to identify changes caused by the activities.

In case of emergency, forecasting the evolving situations will determine the effective resource needed for emergency handling and the conclusion of smart contracts with equipment and people for the implementation of an automatically compiled accident handling plan. This supposes that appropriate 3D models were established, for instance for groundwater bodies, to dynamically assess the impacts and foresee the trend dynamics. This process will also use the selection of optimal traffic routes, visualization, and interactive hints.

Trust based on instant information sharing with all participants and stakeholders will allow keeping the demands of consumers, owners, and responsible parties to the optimal level to protect the rights of future generations up to 2040 and beyond. In this platform, the automation penetrates all project stages and covers the entire life cycle of a mining project up to the closing down of a mining facility and it should include appropriate monitoring of the derelict site up to the time when it can be established with confidence that no negative impact occurs or is likely to occur. Nowadays this needs to include the possible consequences of climate change. A systematic search for resource efficiency and waste management to reduce environmental pressure becomes manageable (Nourani et al. 2019). The integration of transparent economics, governance, environment and company performance, government measures, education, and science will promote the achievement of sustainability goals. The digital platform uses documented, measurable and proven indicators, and the sustainable goals and advancement tasks penetrate all processes of this platform. We can manage only something visible, and management of the demand for energy and metals becomes visualized and manageable only in the digital environment. The service life, maintenance, recycling processes and the reuse of individual components become visible already at the design stage.

It will be imperative to transition to digital technology for gathering, processing, storing, and making available initial and interpreted geological and environmental information, design, operational, financial, market, and social and other data to create a unified source of information on mineral resources.

It is necessary to emphasize the role of public authorities. The ability to accumulate “big data” and use it in building platforms connecting businesses, citizens and the state comes to the fore in science and technology competition. Big data allows you to use your previous experience, knowledge of the whole industry to quickly and efficiently make the right decisions and, thus, to improve the performance of your business processes in terms of time, quality, efficiency, etc. It creates a possibility for sharing knowledge and best practices beyond state borders and political situations for all humanity. Therefore, the distribution structure of knowledge and technology described above is important; independent participants—industry universities and international competence centers—should play a key role in the establishment of such platforms.

Conclusions

The development of the mineral sector requires a significant reduction in the cost of production, the transition to the principles of “lean production,” technological and organizational efficiency improvements. In the context of global inter-sectoral and inter-disciplinary integration, digital technology exerts a growing influence on the development of scientific and technical advances of different sectors. The fourth industrial revolution is causing a rapidly growing demand for certain types of technologies that will increase the competitiveness of mining enterprises.

Establishment of data systems will make it possible:

to obtain geological and economic assessments of the cost and operational effectiveness of investing in the geological exploration and mining;

to evaluate and assess the risks related to safe and environmentally efficient mining;

to manage the performance level, including energy and material resources to optimize costs;

to manage the product life cycle from design to recycling or reuse stage; and

to manage competencies and technological changes in production.

In addition to the need to introduce digital technology and to develop new technological solutions, in the context of the globalization of raw materials markets, it is also important to address the challenge of increasing workforce quality in practically all areas of this market:

by developing and perfecting a system of professional standards for the sector;

by creating a continuous education system to teach the new specialist skills essential for ensuring innovative development within the sector;

by conducting independent assessments and certification of employee skills and qualifications by international standards;

by tracking, forecasting, and alignment of career changes based on competencies and knowledge;

by providing equal access to internships, short-term courses, and case study of technology in the best industry laboratories and centers; and

by providing companies in the sector with incentives to improve employee development programs.

References

Above the Arctic: An intel drone expedition. (2019). Intel. Retrieved January 8, 2019 https://www.intel.com/content/www/us/en/technology-innovation/polar-bears-climate-change.html.

Abramovich, B., & Sychev, Y. (2016). Problems of ensuring energy security for enterprises from the mineral resources sector. Zapiski Gornogo Instituta - Journal of Mining Institute, 217(1), 132–139.

American Association of Petroleum Geologists, Energy Minerals Division. (2018). Unconventional energy resources: 2017 review. Natural Resources Research. https://doi.org/10.1007/s11053-018-9432-1.

Annual Statistics of World Energy. (2018). Retrieved February 27, 2019 https://yearbook.enerdata.ru.

Aqil, M., Kita, I., Yano, A., & Nishiyama, S. (2007). Analysis & prediction of flow from local source in a river basin using a Neuro-fuzzy modeling tool. Journal of Environmental Management, 85, 215–223.

Atlas of Emerging Jobs. (2019). Retrieved February 27, 2019 http://atlas100.ru/en/.

Atomic Expert: Hydrogen energy-the trend of the XXI century. (2018). Retrieved February 27, 2019 http://atomicexpert.com/hydrogen_energy.

Bahga, A., & Madisetti, V. (2016). Blockchain platform for industrial Internet of Things. Journal of Software Engineering and Applications, 9, 533–546.

Benndorf, J., & Jansen, J. D. (2017). Recent developments in closed-loop approaches for real-time mining and petroleum extraction. Mathematical Geosciences, 49, 277–306.

Berman, S. (2012). Digital transformation: Opportunities to create new business models. Strategy & Leadership, 40(2), 16–24.

Beucher, A., Siemssen, R., Fröjdö, S., Österholm, P., Martinkauppi, A., & Edèn, P. (2015). Artificial neural network for mapping and characterization of acid sulfate soils: Application to Sirppujoki River catchment, southwestern Finland. Geoderma, 247, 38–50.

BP Energy Outlook. (2019). https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/energy-outlook/bp-energy-outlook-2019.pdf. Accessed 1 Mar 2019.

Calvo, G., Mudd, G., Valero, A., & Valero, A. (2016). Decreasing ore grades in global metallic mining: A theoretical issue or a global reality? Resources, 5(4), 36–50.

Cascio, W. F. (2019). Training trends: Macro, micro, and policy issues. Human Resource Management Review, 29(2), 284–297.

Central Dispatching Office of the Fuel and Energy Complex of Russia. (2018). Retrieved February 21, 2019 http://www.cdu.ru/.

Christidis, K., & Devetsikiotis, M. (2016). Blockchains and smart contracts for the Internet of Things. IEEE Access, 4, 2292–2303.

Christmann, P. (2018). Towards a more equitable use of mineral resources. Natural Resources Research, 27(2), 159–177.

Dagasan, Y., Renard, P., & Straubhaar, J. (2019). Pilot point optimization of mining boundaries for lateritic metal deposits: Finding the trade-off between dilution and ore loss. Natural Resources Research, 28(1), 153–171.

Deloitte Tech Trends. (2019). Retrieved March 1, 2019 https://www2.deloitte.com/content/dam/Deloitte/br/Documents/technology/DI_TechTrends2019.pdf.

EES EAEC-Private, Information-analytical, Energy Website. (2019). Retrieved March 3, 2019 http://www.eeseaec.org.

EEA. (2018). Environmental indicator report 2018. Resource efficiency and low carbon economy. Environmental protection expenditure. Retrieved March 1, 2019 https://www.eea.europa.eu/downloads/4793507fc36b497dbe6422c884566591/1544193410/environmental-protection-expenditure.pdf.

EIA. (2018). Annual Energy Outlook. (2018). Retrieved March 1, 2019 https://www.eia.gov/outlooks/AEO/pdf/AEO2018.pdf.

Enerdata. (2018). Retrieved March 5, 2019 https://yearbook.enerdata.ru/renewables/renewable-in-electricity-production-share.html.

Ernst & Young. (2013). The use of modern methods of enhanced oil recovery in Russia: It is important not to lose time (2013). Retrieved March 2, 2019 http://npf-its.com/wp-content/uploads/2015/01/Пpимeнeниe_MУH_в_Poccии.pdf.

Fortier, S., Thomas, C., McCullough, E., & Amy, C. (2018). Tolcin global trends in mineral commodities for advanced technologies. Natural Resources Research. https://doi.org/10.1007/s11053-017-9340-9.

Ghassemzadeh, S., & Charkhi, A. (2016). Optimization of integrated production system using advanced proxy based models. Journal of Natural Gas Science and Engineering, 35, 89–96.

Global CIO Survey. (2017–2018). Retrieved January 30, 2019 https://www.logicalis-thinkhub.com/media/1051/21588_logicalis_infographic_171110.pdf.

Global Infrastructure outlook. (2019). Retrieved January 25, 2019 https://outlook.gihub.org/.

Goodenough, K., Wall, F., & Merriman, D. (2018). The rare earth elements: demand, global resources, and challenges for resourcing future generations. Natural Resources Research, 27(2), 201–216.

Gruber, H. (2019). Proposals for a digital industrial policy for Europe. Telecommunications Policy, 43(2), 116–127.

Haines, S., Diffendorfer, J., Balistrieri, L., Berger, B., Cook, T., & DeAngelis, D. (2013). A framework for quantitative assessment of impacts related to energy and mineral resource development. Natural Resources Research, 23(1), 3–17.

Hariharan, S., Tirodkar, S., Porwal, A., et al. (2017). Random forest-based prospectivity modelling of greenfield terrains using sparse deposit data: An example from the Tanami Region, Western Australia. Natural Resources Research, 26(4), 489–507.

Höök, M., Junchen, L., Johansson, K., & Snowden, S. (2012). Growth rates of global energy systems and future outlooks. Natural Resources Research, 21(1), 23–41.

ICMM 2016. Making a positive contribution to the SDGs - Online interactive guidance document on how mining and metals connect with the SDGs. Retrieved January 31, 2019 http://www.icmm.com/sdg.

International Atomic Energy Agency. IAEA Bulletin. (2018). Retrieved January 15, 2019 https://www.iaea.org/sites/default/files/publications/magazines/bulletin/bull/bull592_june2018_corr.pdf.

International Energy Agency (IEA). (2019). IEA 2018 World Energy Outlook. Retrieved January 23, 2019 https://www.iea.org.

International Renewable Rnergy Agency. (2019). Retrieved March 8, 2019 http://www.irena.org.

Jiang, J., Wang, Y., Liu, W., et al. (2018). Multiple regression-based calculation of iron ore resource royalty rate and analytical study of its influencing factors: Example from Anhui Province of China. Natural Resources Research, 27(3), 379–404.

Juliani, C., & Ellefmo, S. (2018). Multi-scale quantitative risk analysis of seabed minerals: Principles and application to seafloor massive sulfide prospects. Natural Resources Research, 28(3), 909–930.

Kathryn, M., Wall, F., & Merriman, D. (2017). The rare earth elements: Demand, global resources, and challenges for resourcing future generations. Natural Resources Research, 27(2), 201–216.

Katuntsov, E. V., Kultan, J., & Makhovikov, A. B. (2017). Application of electronic learning tools for training of specialists in the field of information technologies for enterprises of mineral resources sector. Journal of Mining Institute, 226, 503–508.

Kazanin, O. I., Sidorenko, A. A., & Sementsov, V. V. (2014). Determination of technology parameters of the thick steep gassy seams mining with sublevel caving and coal discharge mining system. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu, 6, 52–58.

Kharas, H., & Gertz, G. (2010). The new global middle class: A cross-over from West to East. In C. Li (Ed.), China’s emerging middle class: Beyond economic transformation (pp. 32–54). Washington DC: Brookings Institution Press.

Krasnov, F., Glavnov, N., & Sitnikov, A. (2018). A machine learning approach to enhanced oil recovery prediction. In W. van der Aalst, et al. (Ed.), Analysis of images, social networks and texts. AIST 2017. Lecture notes in computer science (Vol. 10716). Cham: Springer.

Litvinenko, V. (2019). Russian developments of equipment and technology of deep hole drilling in ice. In Innovation-based development of the mineral resources sector: challenges and prospects - 11th conference of the Russian–German raw materials, 3.

Litvinenko, V., & Meyer, B. (2017). Status and potential for implementation in Russian industry in Syngas production. In V. Litvinenko & B. Meyer (Eds.), Status and potential for implementation in Russian industry (pp. 1–161). Berlin: Springer.

Liu, Y., Peng, Y., Wang, B., Yao, S., & Liu, Z. (2017). Review on cyber–physical systems. IEEE/CAA Journal of Automatica Sinica, 4(1), 27–40.

Makhovikov, A. B., Katuntsov, E. V., Kosarev, O. V., & Tsvetkov, P. S. (2019). Digital transformation in oil and gas extraction. In Innovation-based development of the mineral resources sector: Challenges and prospects - 11th conference of the Russian–German Raw Materials (pp. 531–538).

Månberger, A., & Stenqvist, B. (2018). Global metal flows in the renewable energy transition: Exploring the effects of substitutes, technological mix and development. Energy Policy, 119, 226–241.

McKinsey & Company. (2016). Raw materials: Unlikely return of the 2003–2013 supercycle. Understanding the macroeconomic context and impact on raw materials. Retrieved February 1, 2019 http://www.worldmaterialsforum.com/files/Presentations/PS1/WMF%202016%20-%20PS1%20-%20Sigurd%20Mareels%20Final.pdf.

McKinsey & Company. (2019). Behind the mining productivity upswing: Technology-enabled transformation. Retrieved February 27, 2019 https://www.mckinsey.com/industries/metals-and-mining/our-insights/behind-the-mining-productivity-upswing-technology-enabled-transformation.